Family Offices Could Play a Key Role in the ‘Great Wealth Transfer’

For years, financial advisors have been bracing for the so-called “great wealth transfer” — a cross-generational shift of cash, equities, real estate and other assets older Americans will be handing off to their heirs during the next decade.

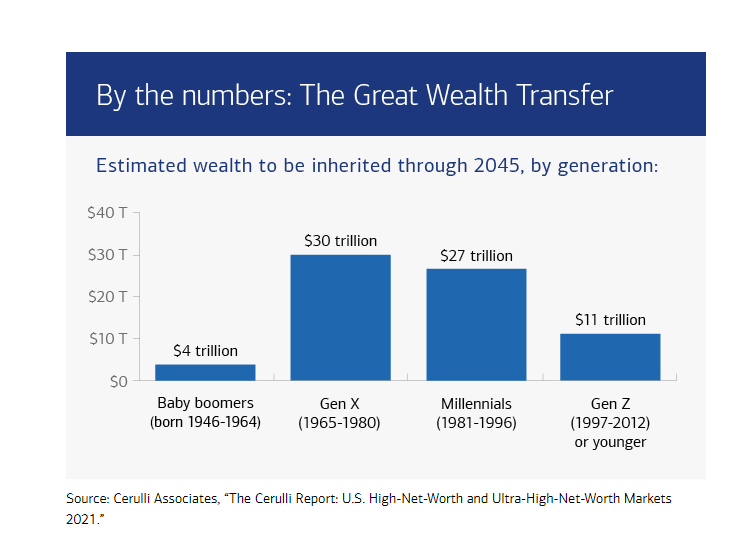

Just how much Boomers will be passing on to their Gen X, Millennials, Gen Z and Gen Alpha heirs is open for debate. While some analysts say the final handoff could be as high as $90 trillion, Merrill Lynch, JP Morgan and others are slightly conservative in their estimations, saying the final tally will be closer to $84 trillion.

Not so fast, says Northwestern Mutual. The insurance giant’s 2024 Planning and Progress Study suggests the long-anticipated, multi-trillion-dollar transfer of wealth has been overblown. It determined that only a “minority of Americans are actually on track to receive a financial gift from their family members,” concluding that about 26 percent of Americans expect to leave behind an inheritance.

The reasons for this unforeseen shortfall are many. Most Americans retire earlier than anticipated, (at 62, according to the Retirement Confidence Survey.) Once retired, many still must negotiate rising healthcare and housing costs, both of which eat away at hard-earned nest eggs. Personal preferences also appear to shape windfalls.

Six-in-10 American parents say their children lack their sense of fiscal responsibility; as a result, 52 percent say this “could negatively impact the family’s assets from one generation to the next.” Meanwhile, 4-in-10 Boomers and two-thirds of Gen X respondents tell Northwestern that they have no will in place because many simply don’t think they will have enough assets to pass on.

How Family Offices Can Help Advise Younger Investors

These findings may come as a disappointment to financial advisors who were eager to help oversee an unprecedented bequeath of assets. But rather than being disappointed that the great wealth transfer may not live up to original projections, advisors should welcome the findings because they underscore the role they play in helping investors manage their assets. This is especially true for family offices — firms specializing in helping high-net-worth clients manage their financial planning. Northwestern Mutual found that only 32 percent of U.S. millionaires consider themselves “wealthy” and 48 percent say their current financial plans need improvement.

This may explain why the insurance company found that nearly 70 percent of high-net-worth individuals are likely to work with a financial advisor, more than twice the percentage — 33 percent — of average investors. High-net-worth clients also place more trust in their financial advisors: 59 percent of high-net-worth individuals value the direction their advisors offer, compared to 33 percent of the general population.

This is especially noteworthy because the wealthiest 10 percent of American households stand to be the biggest beneficiaries of the great wealth transfer, according to the New York Times. Regardless of how much wealth Baby Boomers eventually pass onto younger generations, it will be high-net-worth individuals who both receive the largest portion of the windfall and are most likely to seek out financial guidance.

And — as the cash, equities, real estate and other assets transfer from older investors to younger ones — family offices will likely be dealing with fairly seasoned investors. As the World Economic Forum (WEF) recently found, 70 percent of today’s retail investors are below the age of 45. Yet, despite this experience, the WEF determined that only about 18 percent of U.S. adults between the ages of 18 – 34 possess basic financial knowledge.

In other words, U.S.-based family offices have an important role to play in guiding and educating their younger clients in managing the unprecedented wave of wealth coming their way. Best of all, family offices can take confidence knowing that not only do high-net-worth investors need guidance, but they value it.

Read Susan Lindeque’s thoughts on steps family offices can take today to ensure they remain competitive tomorrow.